This can be a purchase, an increase in the company’s assets, a reduction in income, or an increase in expenses. We call an asset a credit, which can be a reduction in assets, a loan, an increase in income, etc. The entry of a credit in the company’s accounts means that an asset is used.

Salvage Value – A Complete Guide for Businesses

As a core concept in modern accounting, this provides the basis for keeping a company’s books balanced across a given accounting cycle. The accounting equation equates a company’s assets to its liabilities and equity. This shows all company assets are acquired by either debt or equity financing. For example, when a company is started, its assets are first purchased with either cash the company received from loans or cash the company received from investors. Thus, all of the company’s assets stem from either creditors or investors i.e. liabilities and equity. The accounting equation helps in financial analysis by evaluating a company’s current financial health.

- As we previously mentioned, the accounting equation is the same for all businesses.

- Refer to the chart of accounts illustrated in the previous section.

- In other words, all assets initially come from liabilities and owners’ contributions.

- This transaction brings cash into the business and also creates a new liability called bank loan.

- This transaction would reduce cash by $9,500 and accounts payable by $10,000.

- After saving up money for a year, Ted decides it is time to officially start his business.

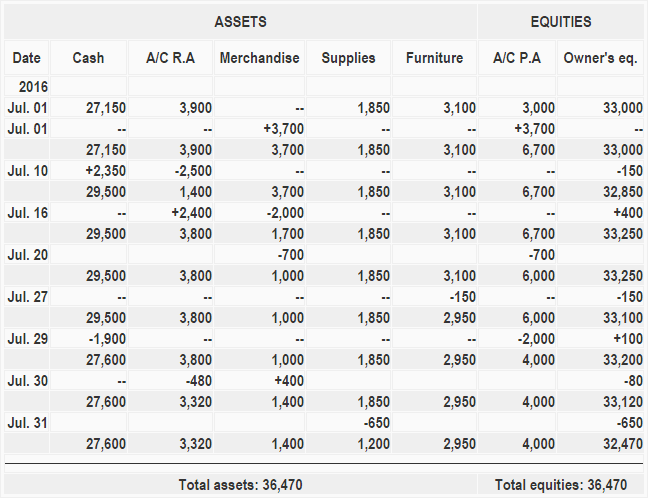

Example Entry for Dual Aspects of Accounting

Profits retained in the business will increase capital and losses will decrease capital. The accounting equation will always balance because the dual aspect of accounting for income and expenses will result in equal increases or decreases to assets or liabilities. Accounting equation describes that the total value of assets of a business entity is always equal to its liabilities plus owner’s equity.

essential elements of the accounting equation formula

As transactions occur within a business, the amounts of assets, liabilities, and owner’s equity change. Consider a company with assets totaling $100,000, liabilities of $60,000, and equity of $40,000. This scenario illustrates the accounting equation perfectly, demonstrating how the components interact. The three primary components of the accounting equation are assets, liabilities, and equity.

What is the Difference Between the Accounting Equation and the Working Capital Formula?

By comparing its assets, liabilities, and equity, you can quickly assess whether a company has enough resources to cover its debts. For example, if a company’s assets are more than its liabilities, it’s a good sign indicating a strong financial position. Additionally, it lays the foundation for a double-entry bookkeeping system, which ensures that every financial transaction is recorded in two places and that the company’s books always stay balanced. On the balance sheet, the accounting equation gives a clear view of financial health by showing how much the company owes and what it owns.

What is Qualified Business Income?

Another example is that the cash obtained (current assets) thanks to a short-term bank loan also represents a debt for the company since it will have to repay these sums, etc. Additionally, adding liability will reduce the value, while decreasing liability, for example, squaring away obligation, will build value. These fundamental ideas are caught by the accounting equation and are vital for current accounting techniques. Although the cash has been reduced, the overall assets remain the same because it has been exchanged for equipment. The total value of the business assets is still $10,000, keeping the equation in balance.

The accounting equation plays a significant role as the foundation of the double-entry bookkeeping system. It is based on the idea that each transaction has an equal effect. It is used to transfer totals from books of prime entry into the nominal ledger. Every transaction is recorded twice so that the debit is balanced by a credit. The accounting equation is based on the premise that the sum of a company’s assets is equal to its total liabilities and shareholders’ equity.

To learn more about the balance sheet, see our Balance Sheet Outline. The global adherence to the double-entry accounting system makes the account-keeping and -tallying processes more standardized and foolproof. Shaun Conrad is a Certified Public Accountant and CPA exam expert with a passion for teaching.

The difference of $500 in the cash discount would be added to the owner’s equity. On 12 January, Sam Enterprises pays $10,000 cash to its accounts payable. This transaction would reduce an asset (cash) and a liability (accounts payable). On 10 January, Sam Enterprises sells merchandise for $10,000 cash and earns a profit of $1,000.

In other words, the shareholders or partners own the remainder of assets once all of the liabilities are paid off. Receivables arise when a company provides a service or sells a product to someone on credit. An asset is a resource that is owned or controlled by the company to be used for future benefits. Some assets are tangible like cash while others is an invoice a receipt are theoretical or intangible like goodwill or copyrights. Now that we know the Debit side has decreased, we need to record the second side of the transaction that will keep the equation in balance. It will always be true as long as all transactions are appropriately accounted for and can never fail or be out of balance for any given entity.

The accounting equation ensures that the balance sheet remains balanced. That is, each entry made on the debit side has a corresponding entry (or coverage) on the credit side. As you can see, all of these transactions always balance out the accounting equation. The expanded accounting equation details how this transaction affects both sides of the equation.

Add comment